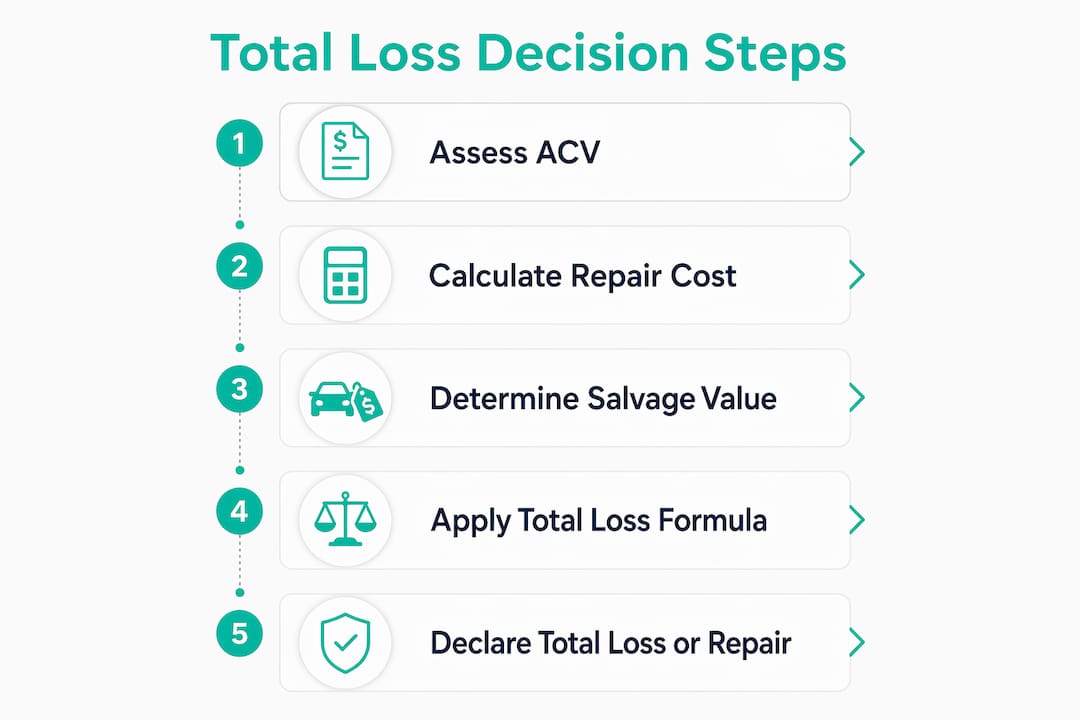

A total loss declaration is defined as an economic decision, not a physical one. Insurers determine whether to repair or total a vehicle by comparing estimated repair costs and salvage value against the vehicle's Actual Cash Value (ACV). Understanding how insurers calculate total loss vs repair is critical for claims professionals and repair shop managers who negotiate these outcomes daily. Two distinct methods govern this decision across the United States: the Total Loss Formula, applied in about 21 states, and the Total Loss Threshold, used in most others. State regulations set the legal framework, but insurers retain significant discretion within those boundaries.

How insurers calculate total loss vs repair using the Total Loss Formula

The Total Loss Formula is the calculation method used when repair costs plus salvage value exceed the vehicle's ACV. When that sum crosses the ACV, the insurer declares a total loss rather than authorizing repairs. About 21 U.S. states apply this formula, making it the dominant method in roughly two-fifths of the country.

The three components of the formula

Each component carries real weight in the final outcome:

- Repair cost estimate. This is the full cost to restore the vehicle to its pre-accident condition, including parts, labor, and applicable taxes. Estimates written under DRP guidelines from carriers like Allstate, State Farm, GEICO, or Progressive must account for OEM procedures and any required calibrations.

- Salvage value. Salvage value is the estimated recovery price an insurer expects when selling the damaged vehicle for parts or scrap. A higher salvage value lowers the effective repair threshold, making a total loss declaration easier to trigger.

- Actual Cash Value (ACV). ACV represents the vehicle's pre-accident market value. It is the ceiling against which repair costs and salvage value are measured.

A concrete numeric example

| Component | Amount |

|---|---|

| Actual Cash Value (ACV) | $15,000 |

| Salvage value | $4,000 |

| Maximum repair threshold | $11,000 |

| Estimated repair cost | $12,500 |

| Outcome | Total loss declared |

In this scenario, repair costs of $12,500 exceed the $11,000 threshold, so the insurer totals the vehicle. If the repair estimate had come in at $10,800, the vehicle would qualify for repair authorization instead.

Pro Tip: When reviewing an estimate in a Total Loss Formula state, always verify the salvage value used. An inflated salvage figure lowers the effective repair ceiling and can push a borderline claim into total loss territory.

What is the Total Loss Threshold method?

The Total Loss Threshold method sets a fixed percentage of ACV as the trigger point for a total loss declaration. Approximately 17 states and Washington, D.C. use this approach, with thresholds ranging from 60% to 100% of ACV across jurisdictions.

A 75% threshold is the most common benchmark. Under that rule, a vehicle with a $20,000 ACV is totaled if repair costs reach or exceed $15,000, regardless of salvage value. The threshold method is simpler to apply than the formula, but it creates wider variation in outcomes depending on which state the claim originates in.

How state thresholds vary in practice

- Alabama: 75% threshold. Repair costs at or above 75% of ACV trigger a mandatory total loss.

- Texas: Damage must exceed 100% of the vehicle's value before a total loss is legally required, giving insurers more latitude to authorize repairs on heavily damaged vehicles.

- States at 60%: A handful of states set the bar lower, meaning vehicles with moderate damage can be totaled earlier in the claims process.

State laws set floors for these thresholds, but insurers can apply lower economic limits to declare total losses earlier when financially justified. That distinction matters for repair shop managers. A carrier may total a vehicle well below the statutory threshold if internal cost modeling supports it.

Pro Tip: Always confirm the applicable state threshold before writing a repair estimate on a high-severity claim. A $14,000 estimate on a $20,000 ACV vehicle may be authorized in Texas but totaled in Alabama.

How do insurers determine Actual Cash Value?

ACV is the single most influential variable in any total loss insurance calculation. A lower ACV makes total loss easier to trigger. A higher ACV gives the vehicle more room to absorb repair costs before crossing the threshold.

Insurers rely on third-party platforms like CCC and Kelley Blue Book to calculate ACV, adjusting for vehicle condition, mileage, and comparable market sales. CCC ONE®, in particular, is the dominant valuation platform used by major carriers including Nationwide and Farmers. The platform pulls comparable vehicle listings from the local market and applies condition adjustments to arrive at a final ACV figure.

What drives ACV up or down

- Vehicle condition grade. Subjective condition adjustments can significantly lower ACV estimates, making it easier for an insurer to declare total loss. A vehicle graded "fair" instead of "good" may lose thousands in ACV.

- Mileage. Higher mileage reduces ACV. Insurers apply per-mile deductions based on market norms for the vehicle's make and model.

- Options and trim level. Factory-installed features like leather seating, a sunroof, or a towing package add to ACV when properly documented.

- Comparable vehicle selection. Choosing weak or inaccurate comparable vehicles is a documented method insurers use to reduce ACV and justify lower total loss payouts. Claimants and repair professionals who identify and challenge poor comp selections often recover meaningful value.

"Discrepancies in pre-accident condition assessments and comp choices are the main drivers of valuation disputes between insurers and claimants. A well-documented vehicle history and a targeted comp challenge are the most effective tools available to claims professionals."

Insurers' selection of comparable vehicles is frequently disputed because it directly shifts the ACV and, by extension, the total loss outcome. Claims professionals who audit ACV reports systematically recover more value for their clients than those who accept the first valuation without review.

What factors push a claim toward total loss beyond the formula?

Insurers view total loss not as whether the car can be fixed, but as a business decision balancing repair cost against car value. That framing explains why some vehicles are totaled even when the math does not strictly require it.

Even repairable vehicles by formula standards can be totaled if insurers predict supplemental claims arising from hidden damage. A vehicle with visible front-end damage may also have frame deformation, airbag system damage, or sensor calibration requirements that are not visible in the initial estimate. Insurers factor the anticipated cost of those supplements into their decision.

Additional considerations that influence the repair vs total loss decision include:

- Supplement risk. Vehicles with complex structural damage carry a high probability of supplement claims. Insurers weigh that risk against the cost of simply paying out ACV.

- Parts availability. Older vehicles or specialty models with limited parts availability increase repair cycle time and cost, pushing the economic case toward total loss.

- Rental exposure. Extended repair timelines increase rental car liability. A total loss settlement closes that exposure faster than a multi-week repair.

- Insurer risk management policies. Individual carriers set internal guidelines that may be more conservative than state law requires.

Pro Tip: When managing a borderline repair claim, document all visible and suspected hidden damage in the initial estimate. A thorough first estimate reduces the insurer's ability to justify a total loss based on anticipated supplements alone.

Key Takeaways

Insurers declare a total loss when repair costs and salvage value together exceed the vehicle's ACV, using either a state-mandated formula or a fixed percentage threshold, with ACV accuracy and comp selection determining the outcome in most disputed cases.

| Point | Details |

|---|---|

| Two calculation methods exist | The Total Loss Formula and the Total Loss Threshold govern decisions across all U.S. states. |

| ACV is the critical variable | A lower ACV makes total loss easier to trigger; always audit condition grades and comp selections. |

| Salvage value shifts the threshold | Higher salvage value reduces the effective repair ceiling in Total Loss Formula states. |

| State laws set minimums only | Insurers can total vehicles below the statutory threshold when internal cost modeling supports it. |

| Hidden damage drives early totals | Anticipated supplement costs push borderline claims toward total loss even when initial estimates fall below threshold. |

Why ACV disputes are where the real money is

I have reviewed hundreds of total loss claims across carriers like State Farm, Progressive, and Allstate, and the pattern is consistent. The formula itself is rarely the problem. The problem is almost always the ACV.

Adjusters working under volume pressure accept the first CCC valuation without scrutinizing the comparable vehicles selected. Those comps are often pulled from adjacent zip codes with different market conditions, or they include vehicles with lower trim levels than the subject vehicle. The result is an ACV that is $1,500 to $3,000 below what the market actually supports. That gap is not accidental. It is structural.

The most effective intervention I have seen is a targeted comp challenge backed by documented vehicle history. Service records, dealer-installed options, and recent inspection reports all support a higher condition grade. When a claims professional presents that documentation alongside three to five stronger market comps, carriers adjust the ACV more often than not. The negotiation is not adversarial. It is evidentiary.

Repair shop managers who understand this process protect their customers and their own supplement recovery rates. A vehicle that gets totaled on a weak ACV is a vehicle that never comes back for the repair. Knowing how to read a valuation report and identify its weaknesses is as valuable as knowing how to write an estimate.

— Izaz

Audenyx supports accurate total loss evaluations

Claims auditing on total loss decisions requires the same rigor as any supplement review. Errors in ACV calculation, salvage valuation, or comp selection directly affect payout outcomes for carriers and claimants alike.

Audenyx provides expert claims auditing for auto damage and total loss evaluations, staffed by certified CCC ONE® professionals trained within DRP guidelines for major carriers including Allstate, State Farm, GEICO, Progressive, Farmers, and Nationwide. With a 12-hour turnaround and 24/7 availability across global time zones, Audenyx gives claims teams and repair managers an independent, audit-ready review of valuation reports, comp selections, and repair cost estimates. When the numbers on a total loss claim do not add up, Audenyx identifies exactly where the discrepancy originates.

FAQ

What triggers a total loss declaration?

A total loss is declared when repair costs plus salvage value exceed the vehicle's ACV in formula states, or when repair costs reach a fixed percentage of ACV in threshold states. The specific trigger depends on the state where the claim is filed.

How is ACV calculated for a total loss claim?

Insurers calculate ACV using third-party platforms like CCC and Kelley Blue Book, adjusting for the vehicle's condition, mileage, options, and comparable local market sales. Condition grading and comp selection are the two factors most commonly disputed by claimants.

Do deductibles apply to total loss payouts?

Deductibles apply differently by claim type. Collision and comprehensive claims deduct the policy deductible from the total loss payout, while third-party liability claims generally do not.

Can an insurer total a vehicle below the state threshold?

Yes. State thresholds are legal minimums, not absolute limits. Insurers can declare a total loss below the statutory threshold when internal cost analysis, hidden damage risk, or supplement exposure makes repair economically unjustifiable.

What is the most effective way to dispute a total loss valuation?

The most effective approach is to challenge the comparable vehicles used in the ACV calculation and provide documented evidence of the vehicle's pre-accident condition, including service records, inspection reports, and dealer-installed options. Carriers adjust ACV more frequently when claimants present stronger market comps with supporting documentation.