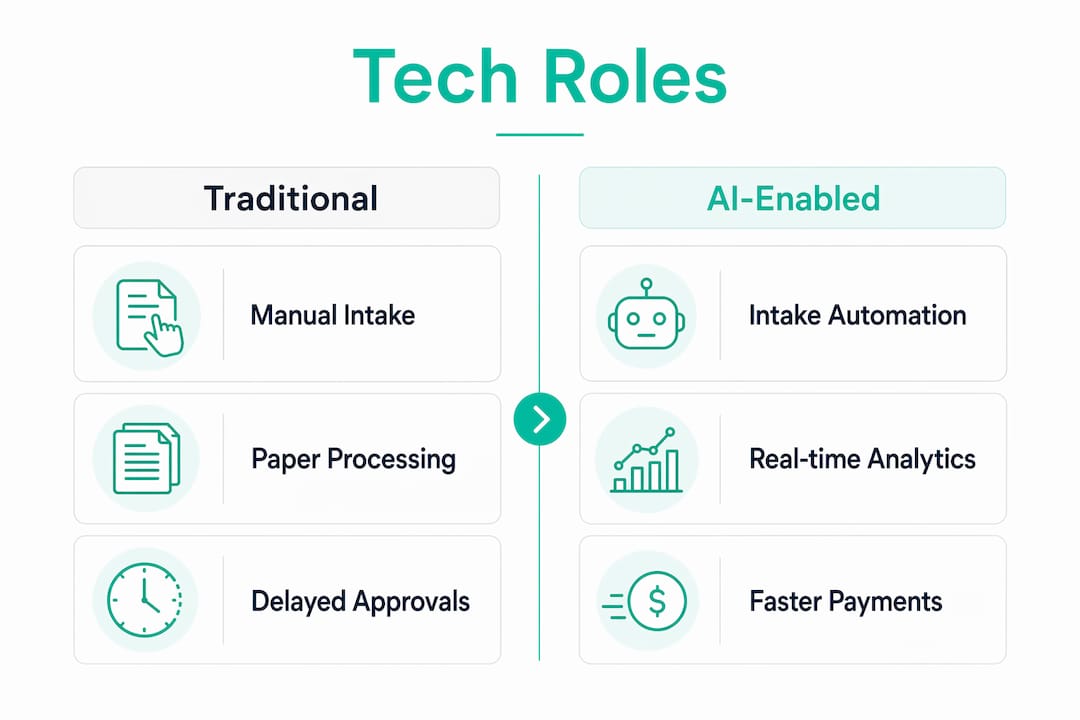

Auto claim cycle time reduction is the process of accelerating every stage of an auto insurance claim, from first notice of loss (FNOL) to final payment, cutting total settlement durations by up to 75% through AI automation and workflow redesign. The industry standard term for this discipline is claims cycle optimization, and it sits at the center of every serious operational improvement effort in personal auto lines. AI-driven automation cuts average claim cycle from 30 days to 7.5 days, a shift that directly reduces loss adjustment expenses and lifts policyholder satisfaction scores. For claims professionals managing adjuster workloads and DRP compliance, the gap between traditional processing and AI-enabled processing is no longer a future concern. It is a present competitive reality.

What does auto claim cycle time reduction require?

Effective cycle time reduction starts with the right technology stack and clean data. Without both, automation produces faster errors, not faster settlements.

The foundational tools fall into three categories:

- AI-driven FNOL intake automation: Captures structured data from photos, telematics feeds, and digital forms without manual keying.

- Optical character recognition (OCR): Extracts text from police reports, repair invoices, and medical records with high accuracy.

- Machine learning decisioning models: Score claims for complexity, fraud risk, and settlement eligibility in real time.

Legacy system integration is the most underestimated obstacle. Most carriers run policy administration systems that were not designed to exchange data with modern AI platforms. Connecting them requires API development, data mapping, and user acceptance testing. Realistic timelines run 14–20 weeks end to end, not the four weeks some vendors advertise.

Clean, structured data input is equally non-negotiable. AI models trained on inconsistent or incomplete claim records produce unreliable outputs. Claims teams must audit their data quality before deployment, not after. Personnel training is the third prerequisite. Adjusters need to understand how to interpret AI recommendations, override them when warranted, and document their reasoning for compliance purposes.

| Technology category | Primary role in cycle time reduction |

|---|---|

| AI intake automation | Eliminates manual FNOL data entry errors |

| OCR document extraction | Speeds document review from hours to minutes |

| ML decisioning models | Automates low-complexity claim approvals |

| Fraud detection AI | Flags suspicious claims before settlement |

| Real-time payment platforms | Enables same-day disbursement after approval |

Pro Tip: Evaluate OCR and AI tools specifically on their surge volume handling capacity. A tool that performs well at average volume but degrades during catastrophe events creates SLA failures at the worst possible moment.

How do you implement AI automation to reduce claim processing time?

A structured implementation sequence prevents the common failure mode of deploying automation in one stage while leaving bottlenecks intact everywhere else.

-

Automate FNOL intake. Deploy digital intake forms, photo capture tools, and telematics data ingestion. This stage alone removes the manual keying step that generates intake error rates of 12–18%, errors that trigger rework cycles running 3.4 times the original processing time.

-

Implement triage and classification. Route claims by complexity score immediately after intake. Simple claims go to straight-through processing (STP) queues. Complex liability cases route to senior adjusters with AI-generated summaries already prepared.

-

Deploy automated decisioning for low-complexity claims. Simple FNOL-to-payment authorization that previously took 5–10 days now completes in same-day to 2 days with AI-enabled processing. That is the benchmark to target.

-

Integrate fraud detection before settlement. Fraud scoring models run in parallel with decisioning, not sequentially. Sequential fraud review adds days. Parallel review adds minutes.

-

Activate real-time payment disbursement. Connect approved settlements directly to digital payment platforms. Eliminating the check-printing and mailing step removes 2–5 days from the tail end of every claim.

-

Redesign adjuster workflows around AI outputs. Adjusters shift from data entry and document retrieval to exception handling and complex case management. Adjuster throughput rises 40–65% without adding headcount when this transition is managed correctly.

Stakeholder communication is as important as the technology itself. Claims managers, IT teams, legal, and compliance officers all need aligned expectations on what automation will and will not handle. Undercommunicating scope is the leading cause of mid-implementation resistance.

Pro Tip: Target a straight-through processing rate above 70%. Carriers that reach this threshold gain a structural performance advantage in expense ratios and policyholder retention that compounds over time.

What causes delays in auto claim processing, and how do you fix them?

The most common delay sources are intake errors, integration failures, surge volume spikes, and unresolved complex liability cases. Each has a distinct fix.

Intake errors are the highest-frequency problem. Manual data entry at 12–18% error rates means roughly one in seven claims enters the system with a defect. Each defect triggers a rework cycle. Rework cycles consume 3.4 times the processing time of a clean claim. The fix is automated data extraction at intake, not downstream error correction.

Integration failures between AI platforms and legacy policy systems cause claim records to stall in handoff queues. The fix is proactive API monitoring with automated alerts when data transfer latency exceeds defined thresholds. Do not wait for adjusters to report missing records.

- Audit integration points weekly during the first 90 days post-deployment.

- Set queue elasticity thresholds before go-live, not after the first surge event.

- Maintain a manual fallback process for each automated stage.

- Track error rates by claim type, not just overall averages.

- Review rework volumes monthly and trace each incident back to its root cause.

Measuring queue elasticity during surge events is more operationally valuable than tracking average turnaround time. Average metrics mask the SLA failures that damage carrier reputation most severely. Build surge capacity into your intake SLA design from day one.

Complex liability cases are the hardest to accelerate. AI can prepare summaries and flag relevant precedents, but human judgment drives the final decision. Realistic expectations matter here. One large insurer cut liability decision time by 23 days using AI-assisted review, but that result required deploying multiple specialized models, not a single general-purpose tool.

Pro Tip: Separate your cycle time KPIs by claim complexity tier. Reporting a single average cycle time hides the performance of your STP pipeline and makes it impossible to identify where delays actually concentrate.

How do you benchmark success in auto claim cycle time reduction?

Benchmarking requires tracking cycle time at each stage of the claim lifecycle, not just the total duration from FNOL to payment.

The core operational KPIs for claims professionals are:

- FNOL-to-assignment time: Target under 2 hours for digital intake channels.

- Assignment-to-inspection time: Target 24–48 hours for standard physical damage claims.

- Inspection-to-estimate time: Target same day for AI-assisted photo estimating.

- Estimate-to-approval time: Target under 4 hours for STP-eligible claims.

- Approval-to-payment time: Target same day with digital disbursement.

| Claim type | Traditional cycle time | AI-enabled target |

|---|---|---|

| Simple physical damage | 5–10 days | Same day to 2 days |

| Standard personal auto | 15–30 days | 7.5 days |

| Complex liability | 30+ days | Reduced by 23 days |

Carriers achieving 70%+ STP rates see permanent competitive advantages in both retention and expense ratios. That is the strategic case for investing in benchmarking infrastructure. Without measurement, cycle time improvements stall because no one can prove where the gains are occurring.

Real-time monitoring dashboards give claims managers visibility into queue depth, error rates, and adjuster throughput on a daily basis. Monthly reporting cycles are too slow to catch emerging bottlenecks before they affect SLAs. The gap between AI-mature carriers and traditional carriers is widening. Benchmarking is the mechanism that tells you which side of that gap you are on.

Key Takeaways

Effective auto claim cycle time reduction requires AI automation across every lifecycle stage, clean data inputs, and real-time benchmarking to sustain measurable gains.

| Point | Details |

|---|---|

| AI cuts cycle time by 75% | AI-enabled carriers reduce average claim duration from 30 days to 7.5 days. |

| Intake errors multiply delays | Manual entry errors at 12–18% trigger rework cycles 3.4 times longer than clean claims. |

| Implementation takes 14–20 weeks | Legacy system integration requires realistic planning, not vendor-promised four-week timelines. |

| STP rate above 70% is the target | Carriers exceeding this threshold gain structural advantages in expense ratios and retention. |

| Benchmark by stage, not total time | Tracking each lifecycle stage reveals where delays concentrate and where gains are real. |

Why sustained cycle time gains require more than technology

The carriers that achieve lasting cycle time improvements share one trait: they treat AI deployment as an organizational change program, not a technology installation. I have seen operations invest in capable AI platforms and still see cycle times plateau within six months. The reason is almost always the same. The models were deployed but never tuned. Data quality was not maintained. Adjusters reverted to manual workarounds because no one reinforced the new workflow.

Aviva's result, where 80+ AI models cut complex liability determinations by 23 days and reduced complaints by 65%, did not come from a single deployment. It came from building an ensemble of specialized models, each addressing a specific stage of the claims lifecycle. That is the architecture that produces durable results.

The next competitive frontier is real-time digital payments combined with predictive analytics that flag potential total losses before the vehicle is even inspected. Carriers that build the data infrastructure now will execute on those capabilities faster than those starting from scratch in two years. Staff training and iterative model tuning are not optional maintenance tasks. They are the mechanism that keeps cycle time gains from eroding. Proactive collaboration between claims, IT, and finance teams is what separates a successful deployment from an expensive proof of concept.

— Izaz

How Audenyx accelerates your claims cycle

Claims professionals who have reduced cycle time at the intake and estimating stages know that audit quality is the next constraint. Inaccurate estimates and missed supplements add days to settlement timelines and leave money on the table.

Audenyx delivers expert auto damage estimating and claim audit solutions with a 12-hour turnaround, powered by certified CCC ONE® professionals trained within the DRP guidelines of major carriers including Allstate, State Farm, GEICO, Progressive, Farmers, and Nationwide. Operating 24/7 across global time zones, Audenyx gives claims teams the audit capacity to match the speed of AI-enabled processing without adding internal headcount. For operations focused on reducing claim processing time at every stage, Audenyx provides the expert review layer that keeps settlements accurate and compliant.

FAQ

What is a good auto claim cycle time benchmark?

The industry average for personal auto claims is 15–30 days. AI-enabled carriers achieve as low as 7.5 days, which is the current performance benchmark for operations with mature automation.

How does AI reduce auto claim processing time?

AI automates FNOL intake, document extraction, claim triage, fraud scoring, and payment authorization. Simple claims that previously took 5–10 days now complete in same-day to 2 days with full AI-enabled processing.

What is straight-through processing in auto claims?

Straight-through processing (STP) is the automated handling of a claim from intake to payment without manual adjuster intervention. Carriers achieving STP rates above 70% gain measurable advantages in expense ratios and policyholder retention.

How long does it take to implement AI claims automation?

Realistic implementation timelines run 14–20 weeks end to end. Legacy policy system integration is the primary driver of that timeline, regardless of vendor promises of faster deployment.

What KPIs should claims teams track for cycle time improvement?

Track FNOL-to-assignment time, estimate-to-approval time, STP rate, adjuster throughput, and error rate by claim type. Reporting a single average cycle time masks where delays actually occur in the pipeline.